If you're getting ready to buy a home this year, there's one important financial detail you shouldn't overlook — closing costs.

While most buyers are aware that closing costs exist, many aren't exactly sure what they cover or why they vary so much depending on where you're buying. Let’s explore the essentials so you’re better prepared when the time comes.

What Are Closing Costs?

Closing costs are the additional fees and expenses you'll pay when finalizing the purchase of your home. Every homebuyer encounters them. According to Freddie Mac, these costs typically include important items like homeowner's insurance and title insurance, along with fees for:

- Loan application

- Credit report

- Loan origination

- Home appraisal

- Home inspection

- Property survey

- Attorney

National vs. Local: Why the Numbers Differ

When researching closing costs online, you’ll often see a national range of 2% to 5% of the home’s purchase price. While that’s a helpful starting point for planning, it doesn’t provide the full picture. Your actual closing costs will also depend on:

- Local taxes and fees (such as transfer taxes and recording fees)

- The cost of services in your area, like title or attorney work

Of course, the price of the home matters, but variations in state laws, tax rates, and local service charges can significantly impact what you’ll pay. That’s why connecting with local experts early on is so important — it puts you in control of your budget before you even start house hunting.

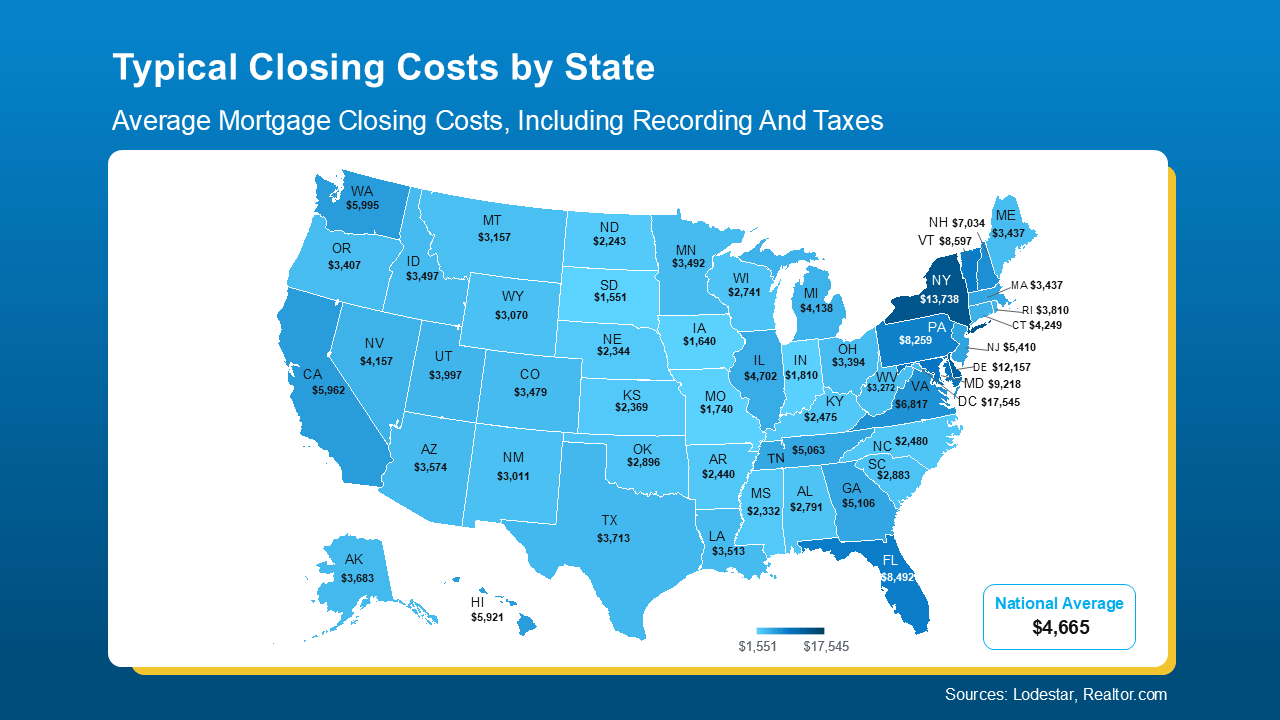

To give you a better idea of what to expect, here’s a state-by-state breakdown of average closing costs based on the median home price in each state (see map below):

As you can see, some states have typical closing costs in the $1,000 – $3,000 range, while others may run closer to $10,000 – $15,000. That’s a wide range, and it’s especially important to know if you’re a first-time buyer. Having a clear understanding of these costs can help you plan more effectively and avoid surprises.

To get a more personalized estimate, your best strategy is to consult a local real estate agent and lender. They can crunch the numbers based on your specific budget, loan type, and location.

Looking for ways to reduce your closing costs? NerdWallet outlines a few helpful strategies:

- Negotiate with the seller. You may be able to ask for a seller credit toward closing costs.

- Shop around for homeowner’s insurance. Compare policies and premiums to find the best deal.

- Look into assistance programs. Some states, professions, or neighborhoods offer financial help with closing costs.

Your agent or lender can help connect you to local resources.

Bottom Line

Closing costs are a vital part of the homebuying process, yet they can vary significantly depending on several factors. By understanding what’s included, knowing what to expect in your area, and exploring ways to reduce them, you’ll be in a stronger position to budget wisely and move forward with confidence.

For personalized guidance and a detailed estimate of closing costs in your area, reach out to Mike Panza and the team at Panza Home Group. They’re here to help you make informed decisions every step of the way. Learn more or get in touch at: https://panzarealestate.com/team/mike-panza