The Federal Reserve (the Fed) is meeting this week, and there’s widespread anticipation that they’ll announce a cut to the Federal Funds Rate. But what does that mean for mortgage rates? Let’s break down what’s really happening and what it could mean for buyers and homeowners.

The Fed Doesn’t Directly Set Mortgage Rates

Many are watching the Fed closely, with economists predicting a rate cut during their mid-September meeting to support economic stability.

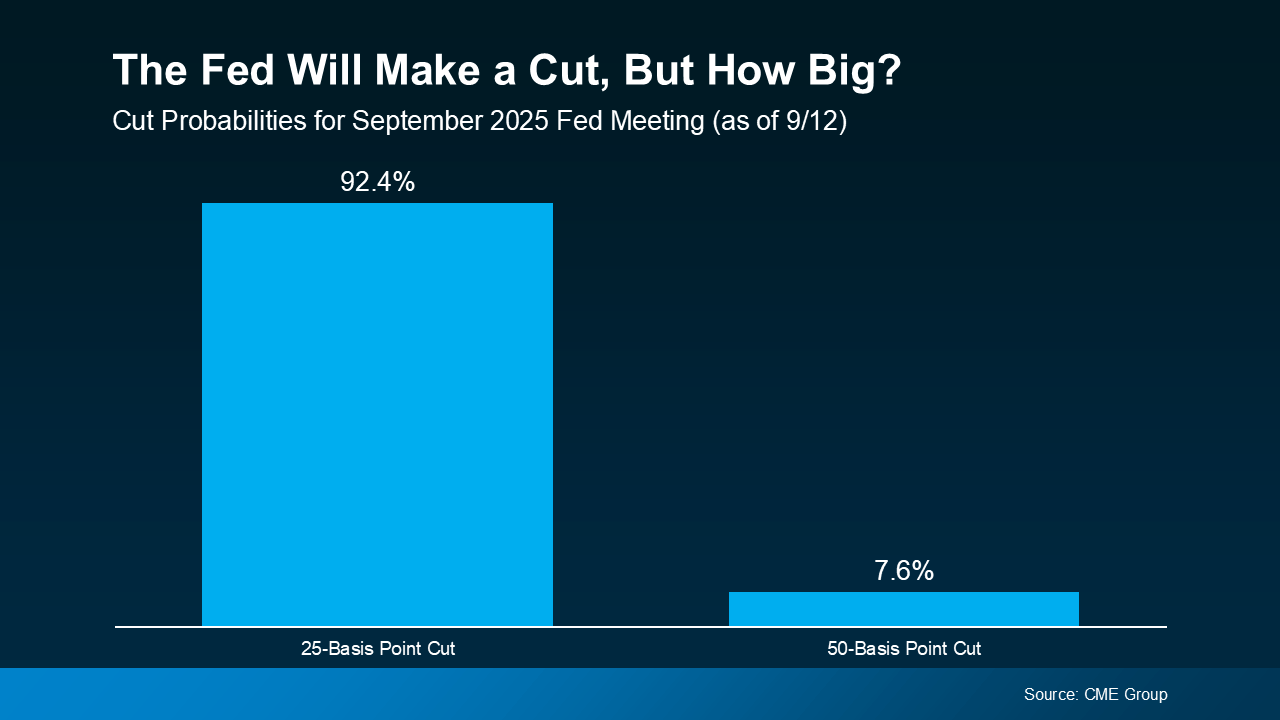

According to the CME FedWatch Tool, markets have already priced in a nearly 100% chance of a cut this September. Most expect a modest 25 basis point reduction, while a smaller segment sees potential for a more aggressive 50 basis point cut.

So, what is the Federal Funds Rate? It’s the short-term interest rate banks use when lending to each other. While it doesn’t directly set mortgage rates, it does influence the broader economy — and that includes mortgage rate trends.

Why Markets Are Already Factoring in a Rate Cut

Here’s some encouraging news: mortgage rates often adjust in advance of Fed decisions. Financial markets tend to price in expected moves before they happen. That means when investors anticipate a rate cut, mortgage rates often begin to fall in anticipation.

That’s exactly what played out after softer-than-expected job reports released on August 1 and September 5. Following those reports, mortgage rates began to ease, reflecting growing confidence in an upcoming rate cut. Even with a slight uptick in inflation in the latest Consumer Price Index (CPI) report, expectations remain strong that the Fed will move forward with a cut.

So, if the Fed delivers the widely expected 25 basis point cut, it’s likely already reflected in current mortgage rates. However, if they choose a more substantial 50 basis point cut, we could see mortgage rates fall even further.

What’s Next for Mortgage Rates?

Even if this week’s cut doesn’t cause a major drop in mortgage rates, there’s still an optimistic outlook.

Many experts believe the Fed may implement multiple rate cuts by year’s end — especially if the economy continues to show signs of cooling (see graph below).

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

That means if the rate-cutting cycle continues — or even if markets simply believe it will — we may see mortgage rates continue to decline gently in the months ahead. Still, the path forward depends heavily on how the economy performs. Surprises in inflation data or unexpected changes could shift these projections.

Bottom Line

Mortgage rates aren’t likely to drop dramatically overnight, nor will they follow the Fed’s rate decisions exactly. But if the Fed begins a consistent rate-cutting cycle — and markets respond accordingly — we may see more favorable mortgage rates later this year and into 2025.

If you’re considering buying or refinancing, now is a smart time to talk strategy. Even modest changes in rates can significantly impact affordability. Understanding what’s ahead can help you make the most informed and confident decision.

For personalized guidance and up-to-date market insights, reach out to Mike Panza and the team at Panza Home Group. They’re here to help you navigate the housing market with confidence. Learn more or get in touch today: https://panzarealestate.com/team/mike-panza.