Buying a home is an exciting milestone — and it might be closer than you think, even when it comes to the down payment.

If you’ve ever thought:

“I’ll never save enough.”

“I need a small fortune just to get started.”

“I guess I’ll just rent forever.”

You’re definitely not alone — but you’re also not out of options.

Here’s the truth: much of what you’ve heard about down payments simply isn’t accurate. Once you understand the facts, you may realize you're in a better position to buy a home than you thought.

Let’s take a closer look at some of the most common down payment myths — and why they don’t have to stand in your way.

Myth 1: “I need a big down payment to buy a home.”

This is one of the biggest misconceptions that causes many would-be buyers to hesitate. In fact, a recent Morning Consult and NeighborWorks survey revealed that 70% of Americans believe they need at least 10% down to purchase a home. Even more surprising, 11% aren’t sure what’s required at all (see graph).

Here’s the good news: According to the National Association of Realtors (NAR), the average down payment for first-time homebuyers has consistently ranged between 6% and 9% since 2018. Even better, there are loan options that require even less. For example, if you qualify for an FHA loan, you may only need a 3.5% down payment. And if you’re eligible for a VA loan, you might not need any down payment at all.

With these kinds of opportunities, the path to homeownership could be easier than you imagined.

Myth 2: “Saving for a down payment takes forever.”

It’s true that saving takes planning and discipline, but reaching your goal may not take as long as you think — especially when you understand what you really need and create a clear strategy.

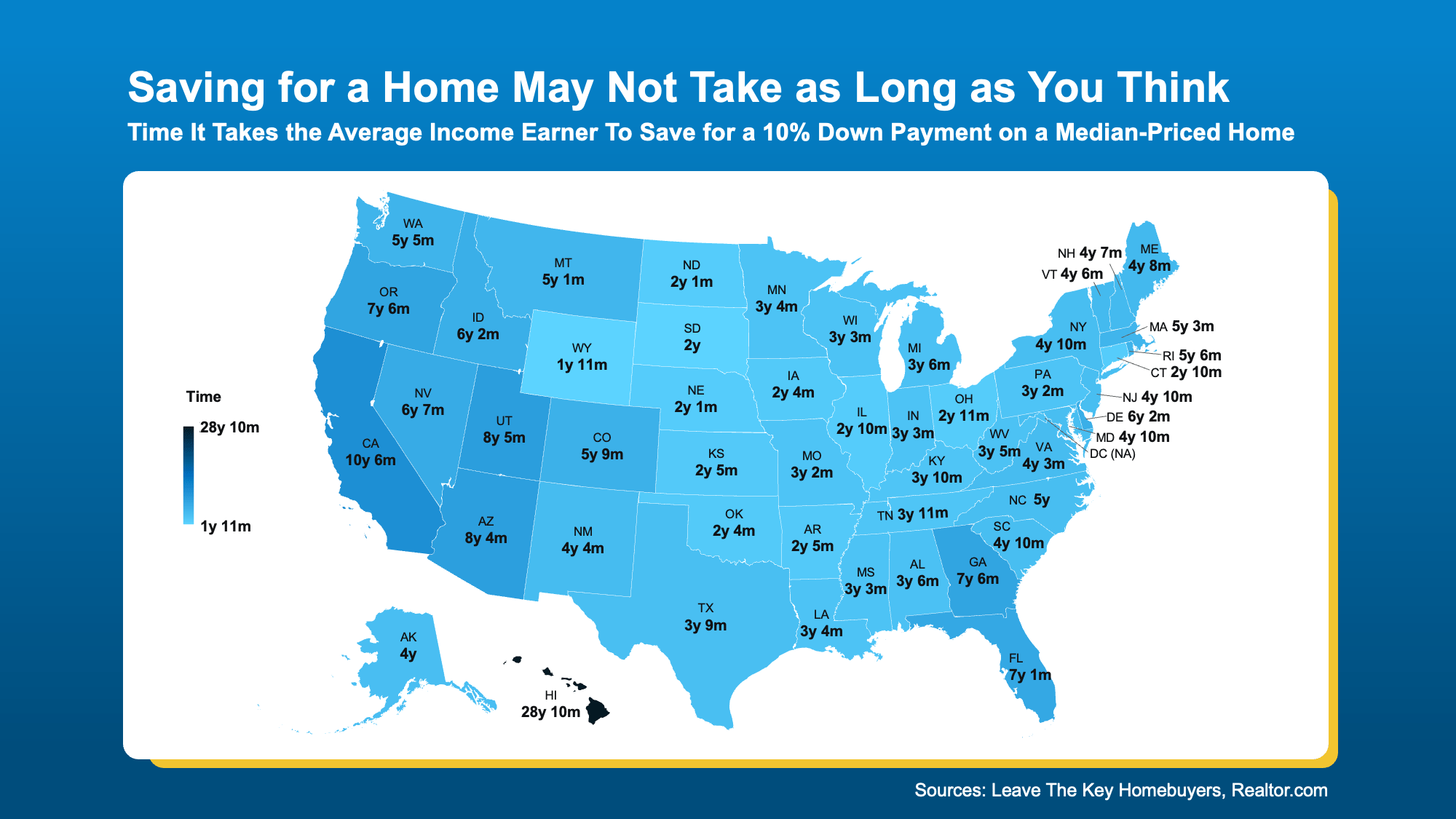

A recent study examined how long it typically takes to save for a 10% down payment in different states, based on average home prices and income levels [see map].

However, you may not even need a 10% down payment. With lower down payment options available, your savings timeline could be significantly shorter. Plus, your entire down payment doesn’t have to come solely from your own pocket — and that brings us to another important myth.

Myth 3: “I have to come up with the down payment all by myself.”

This is one of the most persistent — and most limiting — myths. The reality? There are thousands of down payment assistance programs designed to help buyers just like you. Despite this, the Morning Consult and NeighborWorks poll found that 39% of people aren’t even aware these programs exist.

These programs offer valuable financial support to help buyers cover down payments and, in some cases, even closing costs. As Miki Adams, President of CBC Mortgage Agency, puts it:

“With high interest rates and soaring home prices, down payment assistance is more essential than ever.”

Bottom Line

If you’ve been holding off on buying a home because of concerns about the down payment, it may be time to reevaluate. You could be closer to becoming a homeowner than you realize — and you don’t have to do it alone. From low down payment loans to assistance programs, there are plenty of options to support your journey.

If the down payment wasn’t the thing holding you back, would you be ready to start your home search?

For more personalized guidance on your path to homeownership, reach out to Mike Panza and the team at Panza Home Group. They’re here to help you explore your options and take the next step toward your dream home. Learn more or get in touch by visiting: https://panzarealestate.com/team/mike-panza