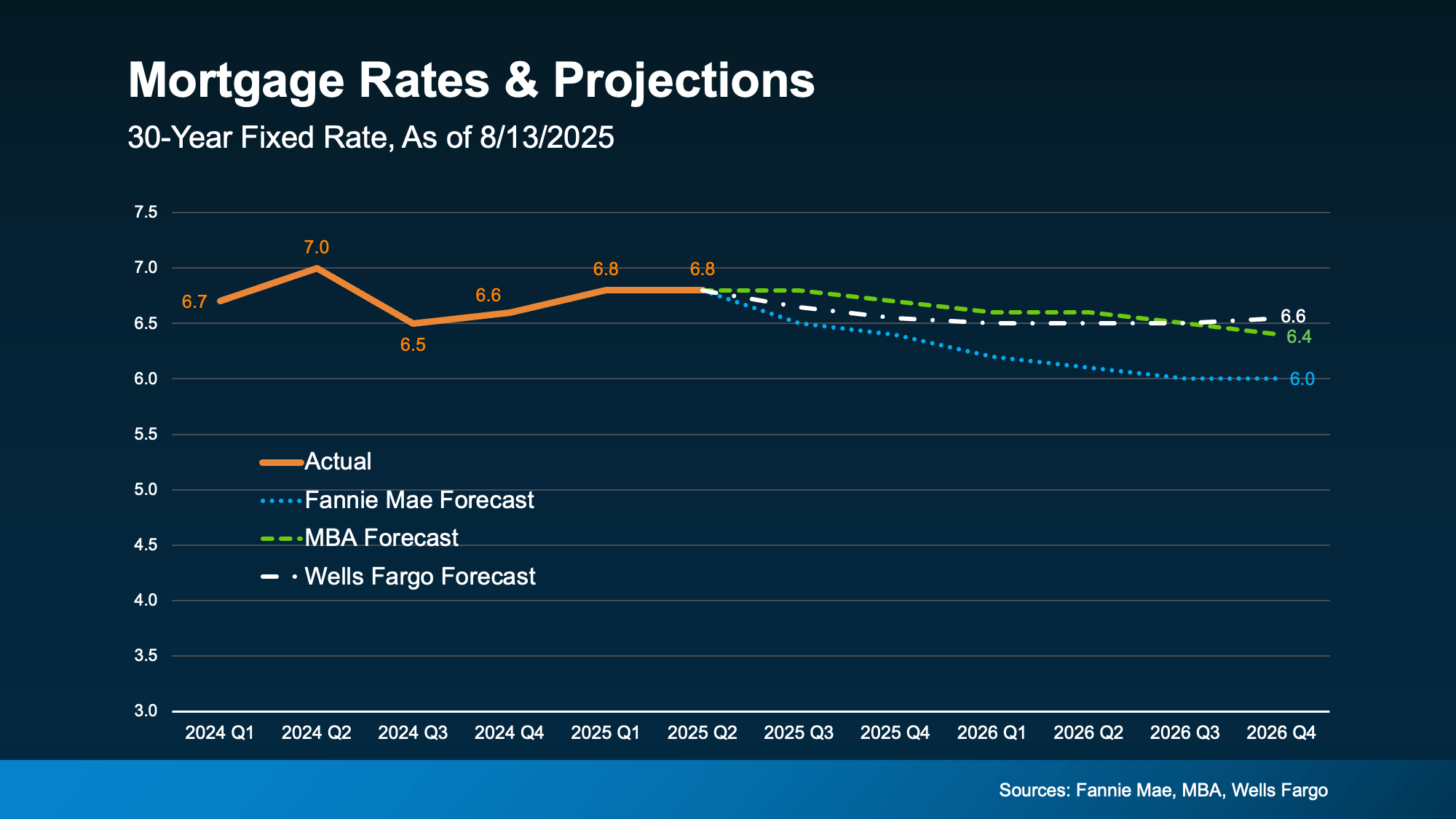

Mortgage rates continue to be a major talking point – and for good reason. Following a weaker-than-expected jobs report, the bond market responded swiftly, leading to a drop in mortgage rates to 6.55% in early August – the lowest level seen so far this year.

While that may seem like a minor shift, it’s encouraging news for buyers who’ve been eagerly awaiting signs of a downward trend. Even a modest dip can rekindle buyer confidence and point toward a more favorable market. But what should buyers realistically expect in the months ahead?

According to the most recent projections, mortgage rates aren’t expected to drop dramatically in the near future. Instead, most industry experts anticipate rates will remain in the mid-to-low 6% range through 2026 [see graph here].

This means while we may not see drastic changes, smaller shifts – like the one we just experienced – are definitely still on the table.

Each new piece of economic data has the potential to influence rates. With multiple economic reports being released this week, we’ll gain clearer insights into inflation trends and overall market conditions – and how those may impact mortgage rates in the short term.

What Rate Is the Tipping Point for Buyers?

The number many buyers have their eye on is 6%. This isn’t just a psychological milestone – it carries real weight. A recent National Association of Realtors (NAR) report shows that if rates hit 6%:

5.5 million more households could afford the median-priced home

Approximately 550,000 potential buyers would likely enter the market within 12 to 18 months

That’s a significant surge in buyer demand just waiting to be unleashed. Encouragingly, if you look at the forecasted rate trends , Fannie Mae anticipates we could reach that 6% threshold next year.

However, this raises an important consideration: does it make sense to wait?

Here’s the Trade-Off

If you’re holding out for that 6% target, it's important to remember you’re not alone. Many other buyers are doing the same. Once rates hit that benchmark, the market could become more competitive, inventory may tighten, and home prices could rise due to increased demand. As NAR puts it:

"Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market."

Right now, conditions may be more favorable than they appear:

Inventory is up = more options to choose from

Price growth has eased = more reasonable pricing

Sellers may be more flexible = greater room for negotiation

These are important advantages that could diminish quickly if mortgage rates continue to drop and buyers flood back into the market. That’s why NAR also notes:

"Buyers who are holding out for lower mortgage rates may be missing a key opening in the market."

Bottom Line

While we may not see mortgage rates reach 6% this year, the current market presents a promising opportunity. Acting now could mean less competition, more negotiating power, and a better selection of homes. Timing the market is always a challenge – but today’s conditions may offer the edge you need before demand picks up.

For more personalized insights on your local market and whether this moment is right for you, reach out to Mike Panza and the team at Panza Home Group. They’re here to help guide you every step of the way.

Learn more or contact Mike Panza directly at: https://panzarealestate.com/team/mike-panza