According to Fannie Mae, 90% of buyers either don’t know the minimum credit score needed to buy a home or think it’s higher than it actually is.

Let that sink in. That means the majority of homebuyers may be assuming they need excellent credit—when in reality, their current score might already be enough. If you’re feeling discouraged about your credit, you could be closer to owning a home than you realize. Let’s take a look at what the data really reveals about credit scores and homebuying.

There’s No One Magic Number

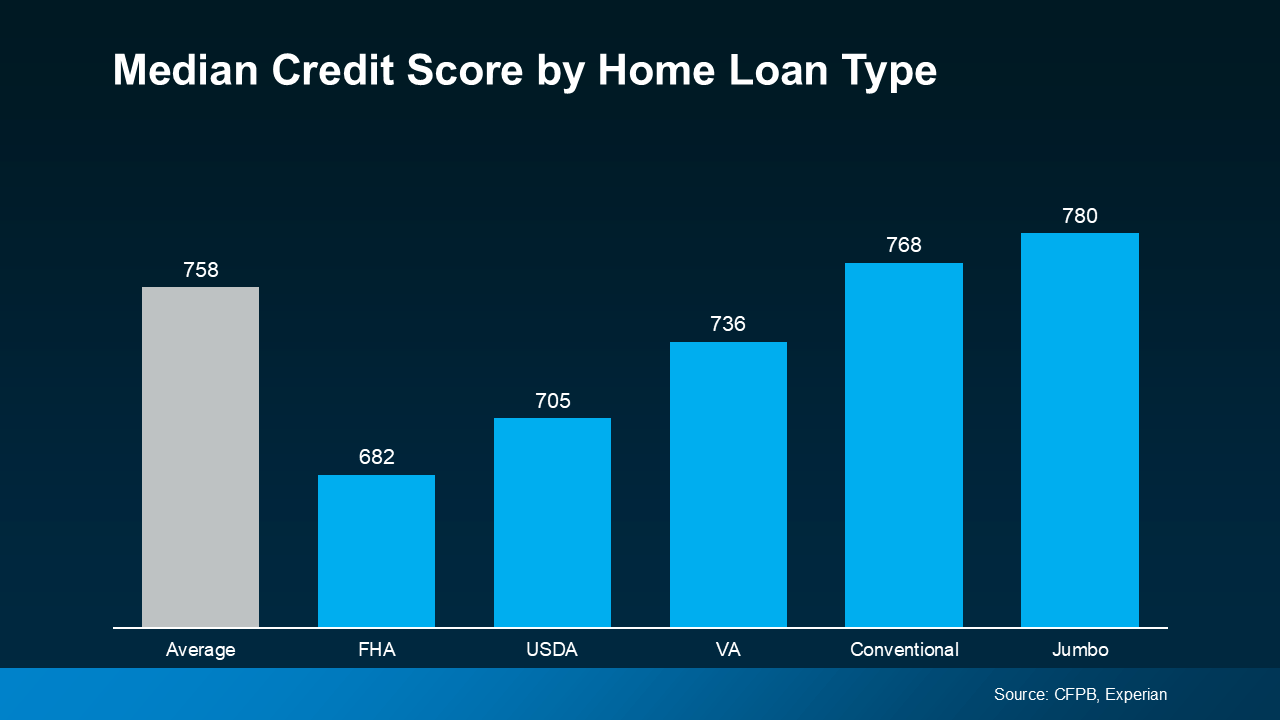

There’s no single, universal credit score that you absolutely need to buy a home—which means you may have more options than you thought. Take a look at this graph showing the median credit scores recent buyers had across various home loan types:

What’s key to understand here is that the required credit score can vary depending on the loan type and the lender. This flexibility means doors may be open that you assumed were shut. The best way to get a clear picture is by speaking with a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Score Still Matters

Even though there’s no one-size-fits-all requirement, your credit score is still a key part of the homebuying process. Lenders use it to assess your financial reliability—whether you make payments on time, manage debt responsibly, and more.

Your score can influence the type of loan you qualify for, the terms of that loan, and your mortgage interest rate. Since your rate affects your monthly payment and overall affordability, it remains a significant factor in your homebuying journey. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

But here’s the good news: you don’t need a perfect score to qualify. Even with room for improvement, many buyers still secure financing and begin their journey to homeownership.

Want To Boost Your Score? Start Here

If chatting with a lender inspires you to improve your credit score—possibly unlocking better loan options and terms—there are some straightforward ways to get started. According to the Federal Reserve Board, here are a few effective strategies:

- Pay Your Bills on Time: This is one of the most important steps. Lenders want to see a consistent history of on-time payments, whether it’s your credit card, utilities, or phone bill.

- Pay Down Your Debt: Try to use as little of your available credit as possible. A lower credit utilization rate can position you as a lower-risk borrower, which may help you qualify for better loan terms.

- Review Your Credit Report: Check your credit reports for errors and work to correct any inaccuracies. This can help raise your score and make you a more attractive candidate for a mortgage.

- Don’t Open New Accounts: It may seem like getting new credit cards would help your score, but applying for too many can actually hurt it. New applications can trigger hard inquiries, which may temporarily lower your score.

Bottom Line

You don’t need a perfect credit score to buy a home. In fact, you might already meet the requirements and not even know it. A better score can help secure more favorable loan terms, but the first step is understanding where you stand and what’s possible. The path to homeownership could be more accessible than you think.

For personalized guidance and to explore your options, reach out to Mike Panza and the team at Panza Home Group. They’re here to help you every step of the way. Visit https://panzarealestate.com/team/mike-panza for more information.